Decoding the Digital Asset Market Structure Draft: What Crypto Businesses Need to Know

Introduction: On May 5, 2025, leaders in the U.S. House of Representatives unveiled the Digital Asset Market Structure Discussion Draft, a sweeping proposal to bring clarity to cryptocurrency regulation. This draft bill — built on last session’s FIT21 Act — aims to draw clear lines between SEC and CFTC oversight, define how and when a token is treated as a security or commodity, and establish new rules for crypto intermediaries. Crucially, it seeks to protect consumers with greater transparency while fostering innovation onshore. Business founders, investors, fintech leaders, and legal teams are watching closely, as this framework could reshape how crypto ventures launch and operate in the U.S. We break down the bill’s key features in plain language — from asset classification to decentralization standards — and examine criticisms, risks, and how the U.S. approach compares globally.

Key Features of the Draft Legislation

Asset Classification — Commodities vs. Securities: The draft clarifies the age-old question: when is a digital asset a security, and when is it a commodity? It introduces the term “digital commodity” to cover crypto tokens whose value depends on the blockchain network rather than a traditional company’s promises. At the same time, it carves out “investment contract assets”, defined as digital commodities sold as part of an investment contract. In simple terms, if a token is sold to raise money (an investment contract), the token itself would not automatically be deemed a security — it could be an “investment contract asset” (a commodity) even though the scheme around it was a securities offering. This is a major shift from the SEC’s past approach of treating many tokens as securities under the Howey test. The bill would amend the Securities Act’s definition of “investment contract” to exclude these tokens, aiming to prevent an asset from being permanently branded a security just because it was used in a fundraising contract. Stablecoins are separately addressed — so-called “permitted payment stablecoins” are explicitly not securities, and are generally treated as digital commodities (with their own forthcoming regulatory regime). Non-fungible tokens (NFTs) are also excluded from the definition of digital commodities in this draft (pending further study). By drawing these distinctions, the bill attempts to bring certainty to token status, though some worry it introduces new definitional complexities of its own (more on that later).

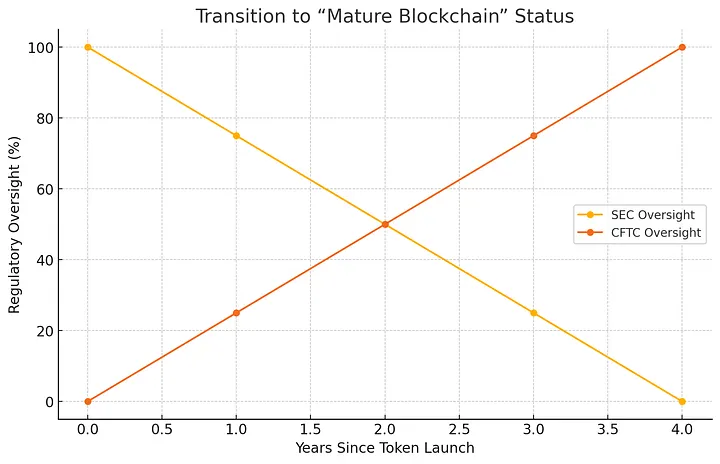

Pathway to Decentralization — “Mature Blockchain” Certification: A centerpiece of the bill is a framework for how a crypto project can transition from a tightly controlled, initially centralized venture to a decentralized network — and how its regulatory treatment changes along that journey. The draft codifies a concept of a “mature blockchain system,” essentially a blockchain network that is no longer under the control of any single person or group. If a project can certify to the SEC that its blockchain is decentralized (“mature”) — for example, no founder or insider has unilateral control or the power to restrict others’ use of the network — then its token could firmly qualify as a digital commodity (under CFTC oversight) rather than a security. The bill lays out criteria and a process for developers to certify decentralization to the SEC. There are statutory conditions for a network to be deemed “mature,” and the SEC is authorized to flesh out further rules on what counts as sufficient decentralization. Notably, the draft would replace the need for ad-hoc SEC “no-action” letters or vague guidance on decentralization with a formal certification process. In the early stages, the SEC is the main regulator (since the project is raising capital from investors), but once the network is certified as mature, primary oversight shifts to the CFTC. During the transition period (up to 4 years from first token sale under the proposal), developers could have a grace period to develop the network, provided they meet certain conditions. Those conditions include disclosure requirements and limits on how much money can be raised ($150 million per year) and on concentration of token ownership (no buyer holding more than 10%). In effect, the bill gives crypto projects a regulated on-ramp: raise funds under SEC oversight, build a functional network, then “graduate” to a decentralized commodity regime. This idea echoes prior proposals like SEC Commissioner Hester Peirce’s safe harbor (which offered a 3-year window for decentralization). Proponents say this “Road to Decentralization” could finally resolve uncertainty for token developers, while skeptics worry about what happens if a project never reaches the loosely defined mature status. (Who decides if a network is truly decentralized, and could bad actors exploit this pathway? These concerns are discussed under “Criticisms” below.)

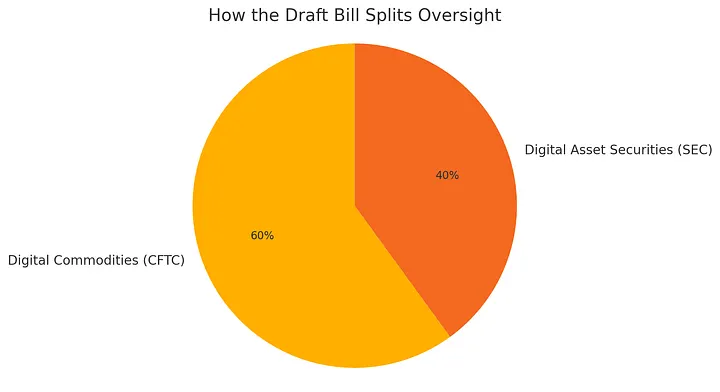

Registration Rules for Exchanges and Brokers: The draft doesn’t just deal with tokens — it creates a regulatory regime for the crypto intermediaries that trade or custody them. In the U.S., trading platforms for non-securities have faced a “spot market gap” with no federal regulator, a gap this bill aims to close. The proposal would give the Commodity Futures Trading Commission (CFTC) new explicit authority over digital asset spot markets, and establish a range of registration categories for market participants. For example, any platform matching trades of digital commodities would have to register as a Digital Commodity Exchange, and brokers or dealers dealing in digital commodities would register with the CFTC as well. These entities would be subject to consumer protection rules similar to traditional securities or commodities intermediaries. Meanwhile, the Securities and Exchange Commission (SEC) would retain oversight of platforms dealing in tokenized securities. To prevent duplication, the bill sets up a system of “dual registration” and notice filings: an exchange or broker-dealer already registered with the SEC can file a notice with the CFTC to operate in digital commodities. Conversely, a CFTC-registered digital commodity exchange could use a streamlined process to offer trading in securities tokens under SEC oversight. The SEC is expressly directed to accommodate crypto trading on traditional securities platforms — for instance, by updating rules to allow alternative trading systems (ATS) to trade digital commodities and stablecoins without being treated as full exchanges. Importantly, the bill includes an interim “notice of intent” process: before formal rules kick in, an exchange or broker can file notice with the CFTC and begin operating under certain baseline consumer-protection standards (such as making token information public, safekeeping customer assets, and filing disclosures) until the final registration rules are in place. This is meant to quickly bring existing crypto businesses into compliance and under regulators’ watch, rather than forcing a shutdown while rules are written. In short, the bill builds a parallel regulatory system for crypto markets: the CFTC for digital commodity trading venues and the SEC for digital asset securities venues, with coordination to avoid overlaps.

Figure: The draft bill divides oversight between the SEC and CFTC. The SEC would oversee crypto securities offerings and related intermediaries (ensuring compliance in token sales, disclosures, and broker-dealer operations), while the CFTC would be the primary regulator for digital commodity trading (regulating spot markets for cryptocurrencies that are not securities). Both agencies would retain anti-fraud authority in their domains, and are instructed to coordinate on rules to minimize duplicative oversight.

Stronger Consumer Protections: A clear intent of the draft is to bolster protections for everyday users and investors in crypto markets, addressing criticisms that the industry has been a Wild West of scams and collapses. The bill’s authors emphasize transparency and accountability as the first line of defense. Crypto project developers would be required to disclose key information to the public, similar to prospectus or whitepaper requirements. This includes details about the project’s technology, governance, tokenomics, who owns and controls the project, and potential risks. In practice, a startup issuing a token would need to publish an offering memo or disclosures that give investors a plain-English overview of how the token works, what it’s used for, and the team’s interests — a step toward traditional investor disclosure norms. Centralized crypto exchanges and custodians would likewise face tighter rules on safeguarding customer assets, business operations, and capital requirements to reduce the risk of another FTX-style meltdown. Notably, the draft explicitly prohibits regulators from banning self-custody of digital assets, cementing the right of individuals to hold their own crypto keys (a response to concerns that heavy-handed rules might outlaw personal wallets). It also extends certain Bank Secrecy Act provisions to crypto brokers and exchanges, treating them as financial institutions for anti-money-laundering purposes. Moreover, the proposal mandates studies on DeFi risks and preserves state consumer protection roles, signaling that this is not a deregulation bill but rather a recalibration of rules to fit digital assets. In the words of the House sponsors, the framework is designed to “protect consumers by strengthening transparency and accountability” while allowing innovation. Requiring accurate public disclosures from token issuers is a core part of that, as is ensuring that customer funds held by exchanges are truly segregated and protected (not used for risky bets). The bill toughens disclosure requirements compared to the status quo, aiming to give investors information “relating to each digital asset project’s operation, ownership, and structure” before they buy in. These measures were informed by lessons from recent market failures and are meant to inject some of the investor protection norms of traditional finance into the crypto space.

Accommodations for DeFi and Innovation: Interestingly, the draft goes out of its way to not stifle decentralized finance (DeFi) development. It includes exemptions for certain DeFi activities from registration requirements, recognizing that regulating a smart contract or open-source protocol like a centralized exchange would be impractical. For example, if a protocol allows users to trade or lend crypto in a self-directed manner without an intermediary (i.e. automated decentralized exchanges or lending platforms), the protocol itself would not have to register as a broker or exchange. The bill defines “decentralized finance trading protocol” in a way that focuses on non-custodial, user-controlled activity. Likewise, simply validating blocks, writing blockchain code, or providing wallets would not trigger registration — these technical activities are carved out so that developers and node operators aren’t unintentionally swept into broker regulations. However, the anti-fraud and anti-manipulation laws still apply in DeFi, meaning the SEC and CFTC can go after DeFi rug pulls or manipulation schemes even if the platforms aren’t registered. The draft also orders a report on DeFi’s risks and benefits to inform future policy. The message is that Congress doesn’t want to drive legitimate innovation underground or overseas by imposing unworkable rules on open protocols. By respecting “disintermediation and decentralization” where it genuinely exists, the bill attempts to strike a balance: protect consumers when there are middlemen handling their funds, but don’t smother software-driven decentralized activity with laws meant for traditional custodians. This delicate approach earned cautious praise from some crypto advocates who note that, unlike previous bills, this one explicitly acknowledges DeFi’s different model. Still, some critics argue that bad actors could label themselves “DeFi” to evade regulations, a challenge that regulators will need to monitor closely.

Criticisms and Potential Risks

While the discussion draft has been applauded by industry for providing a long-awaited framework, it also faces significant criticisms and uncertainties. Opponents range from those who think it gives too many concessions to crypto, to those who feel it still doesn’t go far enough in clarity. Here are some main concerns:

· Unclear or Complex Token Status: Ironically, a bill seeking clarity might introduce new complexity. The creation of new terms like “digital commodity” and “investment contract asset” — with over 15 new definitions in Title I — could invite confusion and regulatory arbitrage. Legal experts point out that tying these definitions to current technology (e.g. defining what a “blockchain network” or “decentralized organization” is in law) could prove quickly outdated as innovation continues. Firms might exploit loopholes by structuring tokens to just barely meet a definition and escape tougher regulation. For example, the draft defines “digital asset” so broadly (any fungible digital representation of value recorded on a public ledger) that a traditional financial instrument like a stock or bank deposit could be wrapped in a token and claim to be a “digital asset” outside normal securities regulation. Critics warn this could allow gamesmanship: companies might put shares on a blockchain and argue they fall under the lighter crypto regime. Additionally, the “digital commodity issuer” concept — identifying a specific entity as the issuer responsible for a token — may clash with how decentralized projects operate (often with multiple entities or none at all). If regulators pin a token to one “issuer” entity, that could actually undermine decentralization, concentrating accountability in a way that crypto projects try to avoid. In short, some believe the draft’s nuanced categories might raise as many questions as they answer, maintaining a degree of uncertainty around borderline cases.

· “Mature Blockchain” and Safe Harbor Risks: The idea of giving projects a safe harbor to decentralize (Section 201’s new Securities Act exemption 4(a)(8)) has drawn fire from investor-protection advocates. Allowing up to $150 million a year in token sales to retail investors under a lighter disclosure regime is seen as very permissive, especially compared to existing crowdfunding limits (just $5 million/year). Over a four-year decentralization period, that could be $600 million raised without full SEC registration — a staggering amount from the perspective of securities law, which traditionally caps private fundraising to protect mom-and-pop investors. The draft does impose some disclosures and requires an “offering memorandum,” but critics note these might be far less rigorous than a true SEC prospectus. Furthermore, the bill allows general solicitation (public advertising) of these token offerings to retail investors without requiring they be accredited. This is unusual, as typically only registered public offerings can be broadly solicited — private offerings are kept limited to prevent widespread harm. Consumer advocates argue that retail crypto investors are just as vulnerable as any, and that letting unregistered token sales reach the public (even with a decentralization promise) could lead to scams or speculative manias. There’s also skepticism about the “decentralization in 4 years” premise: what if developers simply take the money and never achieve a mature network? The bill does not clearly mandate returning funds or unwinding tokens if decentralization fails on schedule. In Commissioner Caroline Crenshaw’s words, every exemption should balance capital formation with investor protection, yet here the scale (up to $150M/year from the public) tilts heavily toward the former. Detractors call this a loophole to sell unregistered securities in the guise of future commodities, potentially creating a Wild West of penny-stock-like token sales. Supporters respond that the anti-fraud provisions still apply and the SEC can crack down on bad actors, but it remains a contentious aspect of the draft.

· DeFi and Enforcement Gaps: By exempting many DeFi activities from registration, the bill acknowledges technological reality — but it may also leave gaps in oversight. Some worry that truly decentralized protocols are rare, and many so-called “DeFi” platforms do have administrators or governance tokens that concentrate power. If those platforms claim exemption, who protects users when something goes wrong? The draft’s approach to DeFi relies on the notion of “self-custody” and user control; however, recent incidents (like algorithmic stablecoin collapses or DeFi hacks) show users can suffer huge losses even without a traditional intermediary. The bill directs regulators to study DeFi risks, but does not yet have a clear solution for how to handle, for instance, a rogue foreign DeFi site accessible to Americans. The SEC’s perspective has been that many DeFi offerings still involve promoters and could be securities. This bill’s more lenient stance sets up a potential clash: the SEC might continue enforcement against what it deems unregistered securities in DeFi, even as the law (if passed) says those activities are exempt. Until final rules and certifications are in place, a gray zone persists — something market participants will have to navigate carefully. Regulatory overlap is another risk: even though the draft directs the SEC and CFTC to coordinate, dual registration could create burdens for companies that have to answer to two regulators. Subtle inconsistencies in SEC vs. CFTC rules (for example, custody requirements or cybersecurity standards) might lead to confusion and compliance challenges. Ideally joint rulemaking will smooth this out, but the proof will be in implementation. Finally, on the political front, there’s risk that this House-led bill won’t survive the Senate or a potential presidential veto. If enacted, it would mark a major shift in U.S. policy — yet opposition from some regulators (SEC leadership) and legislators (concerned about weakening investor protections) could stall or water down the effort. In the meantime, uncertainty continues for projects deciding whether to launch in the U.S. or abroad.

The U.S. Approach vs. Global Crypto Regulations

As the U.S. debates this market structure bill, other jurisdictions have already forged ahead with comprehensive crypto frameworks. Comparing the U.S. draft to Europe, the UAE, and Singapore highlights differing philosophies:

· European Union (MiCA): The EU’s Markets in Crypto-Assets (MiCA) Regulation is often contrasted with the U.S. approach. MiCA, which takes full effect in 2024, establishes a single, uniform set of rules across all EU member states for crypto assets. Unlike the U.S. draft which modifies existing securities/commodity laws, MiCA is a bespoke regime that categorizes digital assets and imposes bank-like safeguards on issuers and service providers. For instance, under MiCA, any company offering crypto services (exchanges, wallet providers) must obtain a license and meet requirements for risk management, capital, and consumer protection. Stablecoin issuers under MiCA must hold sufficient reserves and face caps if their tokens become too widely used, reflecting a financial stability focus. In short, MiCA is a comprehensive license-and-regulate framework: it covers issuance, trading, exchange operations, and even marketing of crypto assets in one package. The U.S. draft, by contrast, splits oversight between agencies and relies on existing definitions of securities vs. commodities, aiming to fill gaps in a more piecemeal fashion. MiCA also explicitly targets market abuse, insider trading, and consumer disclosures, ensuring that crypto-assets not already covered by financial rules (like utility tokens) are still subject to strict transparency and conduct standards. One could say the EU approach is more top-down and uniform — every EU country will follow the same rulebook — whereas the U.S. is proposing a more federated approach using two regulators and carving out nuances like “investment contract assets.” EU officials have touted MiCA as bringing order to crypto markets and protecting consumers and financial stability (noting that many crypto risks originate from the largely unregulated U.S. market). However, MiCA’s heavy compliance costs may push some crypto businesses out of Europe. The U.S. bill’s sponsors likely hope their model proves more innovation-friendly by grafting onto familiar regulatory structures rather than creating an entirely new bureaucracy.